The most recent filing is the court's order granting Intervenor-Respondent Coindesk's Motion to File a Sur-Reply, which is a very procedural element.

Backing up: usually, in court cases, when there's an argument to do something, one party writes a brief, the opposing party writes its brief, and then the first party rebuts the opposing party's brief. Opposing party usually doesn't get a chance to rebut again. This order is letting the opposing party get that chance, and it was done because the first party made new arguments in its reply brief that it's not procedurally allowed to.

The court hasn't rejected Tether's bid to conceal the reserve records... it hasn't reached that point in the case yet. From the current posture of the case, I would guess that it's feeling more sympathetic towards Coindesk than towards Tether, but that really doesn't mean much in terms of what the actual ruling will be.

[1] Any news organization that doesn't provide a link to the actual docket when discussing cases should be considered irresponsible.

Yeah, I had to click through that article, which didn't link the docket, to get to a tweet with an image of a scan of a two-page order granting leave to file. It seems completely unrelated to the headline. Even the word "reject" is the opposite of what happened.

I wouldn't use the word "conspiracy" but just looking at the level of what articles are published doesn't really describe the problem. The top cable news show (tucker carlson) is only watched by 1% of Americans; but the reach of those shows is broader then that. It's human and algorithmic curation that creates the "information monopoly".

Focusing on the human curation, my local newspaper publishes "stories from wire services such as the Associated Press, The New York Times, The Washington Post or Bloomberg News". Even if those individual stories are factually correct and unbiased, I'm only seeing a curated subset of the stories from those outlets. If i rely on my local newspaper as a primary source of information then I'm in their "information monopoly".

Monopoly is a the wrong word here (maybe narrative is a better one) because it's simple to opt out of it. Just admit (or assume) that oneself could be wrong and then actively search out information that proves (or doesn't prove) that you're wrong. Even if you assume people are willing to do this, they probably only have the time and motivation to do so for issues they're passionate about.

That's quite a disingenuous take of what I wrote. It is not in Finbolds or any other news site's interest to include the source, since that makes it easier to write your own article. Now the chances are that they'll become the source instead, so free marketing. It is of course possible to find the source, but if it's not included then basically noone will bother. It increases the barrier just enough to deter most people.

Most people (including myself) are much more likely to read a dumbed-down summary written by a journalist than technical documents that will fly over their head. On the other hand I'm more likely to trust a journalist who cites credible sources.

I would argue it is mostly to deter other news sites. You have done all the work finding this news and then someone else can just come along and write another article based on what you found? You don't want that. But yes the ones "suffering" are the few readers that want to verify the contents.

While there is a glaring lack of references in journalism compared to what is considered normal (or even the bare minimum) in research (academic or otherwise), and that problem is cultural, you don’t have to assume malice to explain it. Like every cultural problem, it is self-perpetuating; but even aside from that, carefully collecting references is simply not the human default.

I once tried to exhaustively document and cross-reference a pretty ordinary coding session of several hours, and took a surprising amount of effort, something like an hour of writing and pasting links from browsing history per two or three hours coding, and you need to do it every two or three hours or else you forget half of what you were thinking. Similar experience with writing down the results of what seemed to be a perfectly harmless week-long dive into mathematical literature.

Annotated bibliographies (let alone anything more detailed) take time and work, which for standard newspaper journalism does not pay off.

I don't assume malice, but I see that a lot of commenters interpreted it that way. My guess is this has to do with the divisive nature of the mainstream media vs alternate media debate? My comment should not be interpreted in that context, I assume both sides don't add sources out of self-interest. They don't want to make it too easy for their competitors to comment on the same news. The barrier is low but it's there. I put it between citation marks because I wasn't really sure what to call it.

I think you also raise an important point regarding culture being a major factor, I agree with that point. Journalism is different from science, so I do not expect the same rigour but I do expect to see the main source in an easily accessible way if possibld (usually a link).

At the risk of igniting a bun fight, perhaps someone with actual knowledge could chime in on the implications of this decision.

My personal, completely unsubstantiated view is that Tether is probably a huge scam. Does this decision force it to reveal whether it is or not, um, or not?

I mean we've seen this play out already, bankers have been forced to open their books due to shady dealings as early as the 14th century. What happens is that banks fall both legitimate and crooked, things get stabilised for awhile, time passes, everybody eventually forgets why such regulations came into being, greed happens again, and this continues on until the present day with the chaos becoming less frequent yet simultaneously spawning hilariously large black swan events.

I don't know how the fine details of all this will shake out, not well enough to make any money off the affair, but I know the rough outline of exactly what is going to happen. Read up on the early history of fractional reserve banking if you'd like to know too.

I don't think anyone knows for sure. There is a decent chance that Tether is (or was before the crash) decently backed by "stuff" - just not with what it claims to be backed by. I'd imagine other crypto holdings were a significant part of it. In other words, it's not really a stablecoin, but some other complex derivative instrument. So it depends on how you define scam. It's certainly false advertising and has always been.

Basically tether mints a bunch of USDT, 'loans' it to bitfinex which then creates an asset on tether's balance sheet of the loan. Bitfinex then goes and buys BTC with the USDT raising the price of BTC.

The problem here is that there is no actual USD anywhere in this system. Net, the system is just one where tether is getting minted out of thin air and then sold to the public for BTC or whatever coins.

The emperor has no clothes, and most crypto seems to be either a scam at worst or delusionally impractical at best.

Bullshit turns to dust in the harsh light of the sun, and i reckon a massive dust storm is what will remain of most tokens that were never really needed for any practical purpose whatsoever, except maybe laundering illegally gotten gains from drugs or corruption, IMHO

I share your opinion, although apparently over the past week Tether's market cap dropped from $83B to $74B which, if true, means that at least $9B have been redeemed in a few days. In other words, they had at least $9B in liquid, USD-convertible assets they could use to redeem those tokens. USDT is currently trading slightly below its peg (around $0.999) and only dipped very temporarily to $0.98 as the cryptocurrency market was crashing.

Now of course they still have $74B to account for and maybe I'm just naive but I have a little more faith in USDT now than I had a week ago, I still think that it's mostly backed by monopoly money but maybe not as much as I thought.

Or alternatively they "redeemed" a bunch of unbacked tokens that they (or a partner company) owned, in order to give the impression that their redemption window was processing large amounts successfully. I'm sure that's not actually the case, but it would be consistent with the "Tether printing unbacked tokens for its own trading" theory of Tether fraud. This may seem like a conspiracy theory, but: the reason these "conspiracy theories" are so easy to believe is that Tether is unregulated and highly non-transparent.

Being only 90% backed by cash isn't the problem. A lot of people could afford to lose 10%, if the money was evenly distributed. Tether would still be a scam in that situation, but it wouldn't destroy the crypto ecosystem.

The risk is that there could be a bank run. People panic and drive down the price trying to get rid of their tether. Now crypto as a whole has lost a lot of the liquidity used to buy/sell crypto. This causes a further panic across other crypto assets.

A dropping market cap absolutely doesn't mean that liquid, easily USD convertible assets were used to redeem them.

It is quite possible that a number of exhanges which had traded IOUs for Tether, Traded that Tether back to have the IOUs canceled.

Edit: Now that I think about it, it really would make sense. They are fighting to keep these records secret, but they may also be cleaning up their books a little in case they lose and have to make their holdings public.

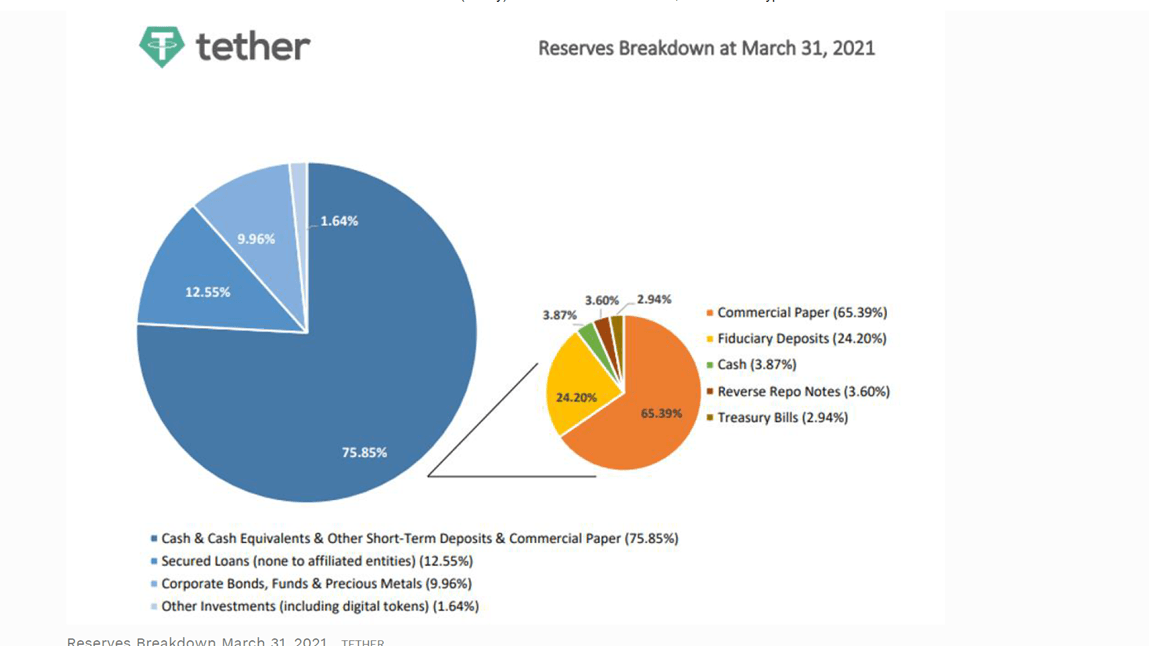

No, all we know is they pushed a button to destroy $9B of Tether, just as they were "printed" in the first place. It says nothing about the transactions behind. From their infamous pie chart their cash reserves are very small (corroborated by Cayman Islands banking stats). It's way more probable they agreed to do it with exchanges to adjust for current customers balances, than Tether the microscopic company transferring real billions of dollars overnight from Cayman Islands through the banking system.

The fact that they so widely advertised themselves as being back 1:1 with USD and then admitted they were lying ruins all their credibility in my eyes.

In addition, I’m surprised so many people defend them by effectively saying ‘this time they’re not lying’ — with no evidence. All I can see it as is wishful thinking than sound judgement.

On the contrary, many of us (as technologists) have a vested interest in shaking out these gambler-creating factions so the rest of the tech may flourish.

Been waiting for Tether to take a K.O. punch for some time, as a cryptocurrency maximalist (eventualist?).

It doesn't really matter at this point. Anyone dealing with Tether either doesn't care or is so ignorant that new revelations won't matter.

Case in point I was buying tether when the peg looked like it was failing a few days ago - so I bought a few dollars for about $0.98. Obviously a tiny trade because I'm not crazy - more for the fun of being able to say I did - but whether the crypto is backed or not was a non-issue. This was to buy a completely different cryptocurrency on a different exchange, and Tether was just a conduit to get fiat money in to the system.

Tether failing might be catastrophic for the crypto ecosystem. It also might not be. Technically speaking, the stablecoins look easy to replace. There is a big test of the whole crypto ecosystem coming to find out how it weathers a recession - total collapse? holds some value? most value? heaven help us, makes money? - which will make for interesting times.

I hate the whole cryptocurrency thing more than most people, but tether may just not be a scam, at least in the legal sense.

Holding their reserves in something other than cash is the way they can make money. The community will consider it betrayal because it essentially relies on the existing system they loath. But other than that, there isn’t too much wrong with it.

That may also point at a reason why they would want to keep this private, which otherwise seems suspicious.

That doesn’t mean people won’t lose all or some of their money with them. Some of these holdings may not be as liquid as needed in a full-on bank run, and they, like all stablecoins, suffer from the mismatch of having no upside by definition but some downside risk.

If Tether held less than $1 in assets for every $1 in circulation...there's a name for what that is...

A bank.

But if Tether is a bank, then UST isn't a 'stablecoin' it's a deposit. And Tether is engaging in what banks have done for centuries, that is increasing the money supply through credit. They are doing it in an illegal and unregulated way which most likely will result in tears and recriminations. But ultimately there is nothing new under the sun.

Edit:

I was wrong in what I wrote above.

Tether is acting as a bank, and yes UST's are simply deposits, but all those people correcting me are right.

Their assets (at least nominally) should match or exceed their libailities.

If Tether holds less than $1 in assets for every $1 in liabilities, it's insolvent. Even banks generally hold at least ~$1.15 in assets for every $1 in liabilities.

But in general, Tether is part of what's known as the "shadow banking" industry--something that quacks like a bank but isn't regulated as if it were a bank. And shadow banking has caused the last several financial crises.

>If Tether held less than $1 in assets for every $1 in circulation...there's a name for what that is... A bank.

Please provide a current example of a bank with <$1 in assets for $1 of liabilities. I ask because if that's how you're defining a bank, that's not (I think) the usual definition.

> held less than $1 in assets for every $1 in circulation...there's a name for what that is... A bank.

I think you are mixing up fractional reserve and assets. Banks have more assets on their books than liabilities, or they are failed/insolvent. Even if tether wants to be a bank (in which case, they should be clear about it) it's not clear that they have the assets in any real sense.

Maybe something in between. Increasing money supply would mean minting USDT out of thin air. Maybe they do, maybe they don't - hopefully the latter.

What they are likely doing is trading that USDT reserves on Bitcoin. Bitfinex is a well known market maker - and a very profitable one. That's probably why they are very much reluctant to disclose their reserves, because they don't have that in cash - unlikely. Knowing how much they own of everything would open the door to critics, and to attacks - the latter is essentially what happened for UST - attackers knew exactly how much cash they needed to depeg UST

A common definition, which happens to better capture my idea of what tether is doing (wrong), is that a bank transforms short-term deposits into long(er)-term loans.

> Holding their reserves in something other than cash is the way they can make money

Depending on what it is, that's also a way they can lose money.

If you think of Tether as an investment organisation that takes $ and hands out claims which they say are worth 1$, while making a bunch of investments, what's that in regular investment land? A money market fund. What can go wrong? https://www.investopedia.com/articles/economics/09/money-mar...

Yes; I think that's absolutely right and insightful - the right way to think about Tether is that it's an opaque (refuses to disclose asset mix; is not audited), expensive (pays no interest; charges for redemptions), unregulated (not subject to the SEC or any other regulatory body) money market fund.

In the real world, literally no-one would own that.

You can in theory hold it off-exchange and transmit it without KYC, which has to imply a certain category of use. But most of it is being used as the "float" by exchanges, I believe.

That depends. If their holdings are in slightly risky "paper" to make money then it's not truly a stable coin because it relies on the market not going down, as it is doing right now. For example, if half their paper is in something roughly indexed to the Dow or similar then their backing is down roughly 5% YTD. That effectively means their actual peg is worth $0.95 on the dollar, a shakeup that could put them into a downward spiral.

On the other hand if they're exclusively in something as safe as US Treasury notes, satisfied by profiting a very small % but on a large pile of money, then they're on more solid footing. The fact that they say "commercial" paper makes me doubt this somewhat.

TLDR: if their 100% backing is in anything with even moderate risk, they could be doomed.

Well, Tether periodically breaks down their assets a little more, so we know that on December 31, 2021, Tether held ~$5 billion in cryptocurrency. Given that at the same time, Tether had just ~$140 million excess assets over liabilities, we can already conclude that Tether is probably insolvent solely from the subsequent rout in cryptocurrencies.

My suspicion is that a large fraction of Tether's claimed assets aren't valuable at anywhere near Tether's claimed value, and so Tether has actually been insolvent for years, and this is the main fuel for their reluctance to be precise in what their asset pool looks like.

7 or 8B were redeemed yesterday within 24 hours, not bad isn't it? This goes without saying that it's only 10% of the market cap, but still better than many banks ...

Speaking of banks, another question: which legacy bank would be able to redeem all money of all account holders? the answer is: none. The money you have on your account is "safe" only because there is no panic. Does that make traditional bank a huge scam?

Tether's liquidity position keeps getting compares to banks, as though banks hold 10% of all reserves and nothing else

They hold 10% in _cash_, and 90% in debt. That debt is liquid and can be traded for more cash easily in the case of a bank run (possibly even guaranteed by the fed?)

Tether _may_ be holding cash and assets covering 100% of its reserves, but 1) it's not sure, 2) it's not clear how liquid those assets are (e.g. dubious CP)

If Tether hold cash+assets covering 90% of issuance then it's a scam. If they hold 99% then it's a scam. It's not equivalent to fractional reserve banking

> which legacy bank would be able to redeem all money of all account holders? the answer is: none.

That answer is correct only in a very limited sense. All legacy banks have more assets than (non-equity) liabilities. In addition to that, banks have liabilities with lower seniority than deposits, which take losses before deposits. So yes, if a healthy bank faces a liquidity crisis, all deposits can't be paid out immediately. But they can be paid in full after the assets are liquidated. That's why banks are not huge scams. They are machines that create long term lending from short term borrowing, which actually is a useful thing. And yes, that contains many known risks, which is precisely why banks are regulated and audited. (I have yet to hear an understandable explanation how a mortgage or business loan works in crypto world - without fractional reserve banking, that is.)

What potentially makes stablecoins scams is if they do not have assets to cover their liabilities. And funny thing is, that would be extremely easy to show to be not the case by being open about the details of the reserves. So easy, in fact, that it is practically impossible to come up with any other reason for not being open about the reserves than them actually being scams.

That's exactly why traditional banks are subject to heavy oversight and regulations, and deposits are protected by govt guarantees. Tether on the other hand is operating completely in the dark and has been involved in a lot of shady activity that does nothing but undermine trust in their ability to do treasury operations in a responsible manner.

1) Banks are solvent. Assets exceed liabilities. They have a liquidity problem if there is a bank run, but can unwind there position and pay all account holders if given enough time to do so. (To be clear, it is still possible for a bank to go insolvent)

2) Historically, bank failures and bank runs were a major recurring problem. Our current financial regulations are written in the blood of those past failures.

3) Among the many safegaurds in place is the FDIC, which insures depositors against bank failures. The FDIC is backed by the US government.

There are two different failure modes for Teather

1) A liquididy problem (bank run). Teather pauses redemptions while until it is able to liquidate its other assests. Might cause a panic, but long term, your Teathers can still be redeamed for dollars. If their is trust in the market about this, 3rd parties can provide liquidity as a form of arbiteage (causing the value to dip below $1, but not crash)

2) A solvency problem. Tether runs out of money and the remaining holders get 0. Or, Tether knows they haveva problem and pay everyone pennies on the dollar.

I wanted to make a comment explaining how banks are different because they lend that money back out - it's not like they don't have it, they just don't have it liquid. Regulations are very strict about what percentage they must keep available. Also there's things like FDIC insurance. But at the of the day they are something akin to a government sanctioned ponzi scheme. It's true that if everyone asks a bank for their money back at the same time, the bank will fail.

I imagine you're bringing this up to say that crypto is no worse than traditional banks. I disagree strongly with that.

Also, it's not even that debt isn't liquid; debt (much like corporate stocks, bonds, etc.) is very liquid. It's just not something you want to be forced to exit prematurely.

So it's not even that the bank can't pay out, it's just that it costs them a little extra.

It's a fair point, I also view banks and fractional currency as slightly scammy, but subtly, not outright.

One difference is that there are apparently strict rules that banks and central banks are supposed to follow (though the rules seem to change or bend expediently), and they are backed up by the government ('bailed out') if they screw up.

Also the Tether people themselves do not appear to be revered for their integrity.

a) Banks have actual rules they have to follow with respect to fractional reserves.

b) Individual bank accounts (in the US) are backstopped by the federal government, via FDIC. It might still be a scam, but it's a scam whose validity is backed by the most expensive military on Earth.

Every legacy bank can redeem all of the money their account holders have in a single day, they don't have the cash on hand but the federal reserve is there on hand to provide liquidity to any solvent bank. The whole framework of oversight and regulation is what makes it possible for banks to have this backstop.

Tether says 7 or 8B were redeemed yesterday. But nobody can actually verify that even those redemptions were processed for real cash. All we know is that Tether is very heavily advertising the notion that their redemption window is working great.

Whats your source for this claim?

If the redeeming parties are associated with Tether/Bitfinex, I would highly doubt that the money is actually going back into the regular financial system.

I fully think there's something shady going on, but the best “devil's advocate” opinion I can come up with is that stablecoins are in a pretty precarious legal position wrt. money laundering laws, and knowing which institutions they bank with gives the US government more parties to put pressure on.

> Top five accounting services firm Grant Thornton LLP issues attestations each month on the US dollar denominated reserves that back the USDC tokens in circulation.

One reason is that Tether is not a US company and does not itself operate in the USA. Submitting anything to a US court is a willingness to be subject to US rules and laws.

Tether is used by Americans, transacting with Americans on American soil, pegging itself to the American dollar, using American dollars as reserves, using the internet which is controlled by America, holding reserves in a banking system largely controlled by America...

Tether.to lists a US address and phone number. Their ip returns a cloudflare ip in California.

They are definitely subject to US law. Pretty sure the US could do things like have them arrested in their home countries, extradited, have their bank accounts seized, etc. I suspect the US could also seize all US dollars without the consent of any foreign nation as well, seems like a natural way to defend a currency. Hard to claim you're backed by US dollars in that case.

> why wouldn't they want to share these documents? Are these trade secrets or something similar?

Playing devil’s advocate, their users clearly don’t care if they’re backed. As such, they’re running a hedge fund with zero cost of capital. Those typically have good reasons for treating their strategies as proprietary.

> My personal, completely unsubstantiated view is that Tether is probably a huge scam.

Tether's not really doing anything different from the what banks do every day. If it crashes the government should just bail them out like they did with the banks in 2008. They will spare banks from the consequences of their actions, so there's no reason why they can't do the same for Tether.

Also: the banks were expected to and did pay it back collectively, with profit.[0] I don't see how Tether could do that if it turns out the fundamentals are bogus.

You'd think Tether would be in favour of something like this as an investor confidence thing but they aren't. I struggle to understand how that can be without it throwing some doubt on the viability of tether itself. Does anyone know how to square this circle?

finance is huge on secrecy, because the moats are often non-existent and often strategies can be replicated trivially.

ask your own pension fund to show terms of every deal they make with your own money. they'll tell you to take a hike, and tether isn't any different here.

Are you sure? Because my pension fund (ABP) has this page: https://www.abp.nl/over-abp/duurzaam-en-verantwoord-beleggen... I found it as result #1 when googling ABP investments. As you can see there are several PDFs listing investments of each category:

- External fund managers

- Engagements with companies

- Overview corporate bonds

- Overview nation-state bonds

- Stocks

- Overview top 100 largest investments

All contain detailed lists about the country, instrument invested in, sector and how large the stake is rounded to the nearest million euro. All these lists are updated regularly as changes occur. Nobody is asking Tether to disclose every term of every single deal they make, but making disclosures about the composition of your underlying assets is not a very big deal at all. You can find similar documents for almost every pension fund out there.

full legal agreement of their mandate publicly available to the entire world, Y/N?

>Engagements with companies

full legal terms of engagement public and available to the entire world, Y/N?

You are just listing some public information. Actual source of alpha is a very closely guarded trade secret, and will never be made available to you, or anyone not involved directly.

Tether is literally being asked to openly disclose confidential business information to the entire world.

They've revealed composition a number of times, they have done an attestation, and none of the other stablecoins have produced an audit either.

That report lists every single bond they have down to the dollar and maturity rating. It lists every hedge fund, vc and other private equity they have on their books.

That’s what is normal (and in the us required) for pensions.

That you have a different expectation for reporting than other market participants doesn’t make it a witch hunt, quite the opposite your standard is much much lower than average.

It’s a MBS that went to zero as part of the 2008 troubles. The underlying mortgages for it are no longer available because it and the company that sold it are gone. Before the default mbs prospectuses listed the mortgages in each tranche along with metadata like type, credit rating, etc.

Your turn. Can you find a single bond trader who has sold “commercial paper” backing tether? I’ll take a journalist who has talked to one as well.

PS: I’m not a beneficiary of calpers, this is public information available to anyone. My private retirement funds and money markets all offer at least this much information in their documentation if not more.

> Tether is literally being asked to openly disclose confidential business information to the entire world.

If what you are invested in is confidential business information, you're doing something wrong. This is all the more true because Tether's claimed value to its customers isn't "you're going to make bucketloads of money if you invest in my fund" but "invest $1 in my fund and you can get $1 (no more and no less) out at any time." Given the latter goal, the fact that it took an awful lot of teeth pulling to get Tether to reveal as much detail as it has should be a massive red flag of risk.

> what is the big issue? money market funds your pension invests in have the same composition as Tether.

We're asking for the same transparency as every money market fund in existence. Why should that be so hard for Tether?

Go to https://www.fidelity.com/mutual-funds/mutual-fund-spotlights.... Pick any fund. Look at the prospectus. Note that there is a link to the "Monthly Holdings Report." [1] Which is a list of every single investment the fund makes, including the CUSIP (basically serial ID) of every bond.

If people aren't willing to tell details on what you're invested in, that is considered one of the red flags that you're investing in a Ponzi scheme.

[1] I'd link directly, but the final link is a downloaded PDF, so it's not as easy to copy the link.

I have a financial advisor who does all this for me so as it happens I have 100% clarity regarding what my retirement funds are invested in. Asking a financial services provider to prove they've got the assets they say they have is absolutely table stakes and even required by law in a lot of cases. But not for crypto scams, of course.

They will tell you to take a hike because you will see that pension fund managers have been obviated by broad market index funds with 0.03% expense ratios and there is no reason to pay a pension fund manager anymore.

So if they really had some magic investment strategy why waste it only on storing backing for stable coin? Why not just run it in proper hedge fund or similar and rake even more money?

> Why not just run it in proper hedge fund or similar and rake even more money?

Because hedge funds sometimes collapse, and Tether's original premise was that being something that couldn't happen. It's why they promised every $1 worth of USDT corresponded to $1 USD in a bank account, prominently on their website, for several years after that stopped being true.

Bernie Madoff paid out when people wanted to withdraw, too. Until he couldn't.

Fruads often look healthy on the outside right up until the collapse. No one's arguing Tether holds no assets, but they've been very cagey - and frequently, outright fraudulent - about whether they hold enough for their stated model.

If Tether was backed 1:1 with Bitcoin, and Bitcoin sank 50%, Tether'd be able to redeem half of their Tethers without an outward indication of issues. "See! We're fine, we're paying out all requests!"

> The OAG’s investigation found that, starting no later than mid-2017, Tether had no access to banking, anywhere in the world, and so for periods of time held no reserves to back tethers in circulation at the rate of one dollar for every tether, contrary to its representations. In the face of persistent questions about whether the company actually held sufficient funds, Tether published a self-proclaimed ‘verification’ of its cash reserves, in 2017, that it characterized as “a good faith effort on our behalf to provide an interim analysis of our cash position.” In reality, however, the cash ostensibly backing tethers had only been placed in Tether’s account as of the very morning of the company’s ‘verification.’

> On November 1, 2018, Tether publicized another self-proclaimed ‘verification’ of its cash reserve; this time at Deltec Bank & Trust Ltd. of the Bahamas. The announcement linked to a letter dated November 1, 2018, which stated that tethers were fully backed by cash, at one dollar for every one tether. However, the very next day, on November 2, 2018, Tether began to transfer funds out of its account, ultimately moving hundreds of millions of dollars from Tether’s bank accounts to Bitfinex’s accounts. And so, as of November 2, 2018 — one day after their latest ‘verification’ — tethers were again no longer backed one-to-one by U.S. dollars in a Tether bank account.

Then, On May 10, 2019 "To alleviate the cash shortfall, BitFinex announced it would conduct a private offering for $1 billion for it's token Unus Sed Leo."

SBF, a crypto insider, has said these issues are the growing pains of a company not allowed to use the US banking system and suck with second and third tier banking solutions.

> In its recent subpoena application, Bitfinex claims that these losses were the result of theft or criminal mismanagement by Crypto Capital. Without signing a formal agreement, Bitfinex entrusted $880 million with Crypto Capital and since then has been unable to access it. In a bid to avoid disclosing these difficulties to its users, Bitfinex initiated the scheme to “borrow” money from Tether.

You think this makes them look less sleazy? Who gives someone nearly a billion dollars without a contract?

The early days of crypto were an under-regulated wild west but most projects are now moving from sleazy to more formal regulation. There is evidence that Tether is making moves to improve.

The fact the NYAG settled for $18.5M is as concrete as it gets. If there were more wrong doing than a frozen bank account, why would NYAG settle with no wrongdoing admitted?

A whole bunch of very guilty companies have settled “with no wrongdoing admitted”. That’s entirely standard. If that’s your only evidence of turning things around, ooof.

Clients have successfully redeemed 10% of outstanding USDT, which happens to be the fractional reserve requirement for major US banks. Evidence they are at least as liquid as any US bank is required to be.

https://www.investopedia.com/terms/f/fractionalreservebankin...

Tether is nothing like Bernie Madoff (not an investment or path to riches) and everything like a state issuing currency. As long as the core constituents have a stake in it (the elite exchanges), then it will go on with out issue.

The risk to Tether is not default, a but an attack.

By creating the stablecoin they got the funds to play with (invest, I mean...) Without it, they wouldn't be able to raise a simar amount without being more strictly regulated.

Because you never want the value of your portfolio to never be less than the stablecoins you issued. If you are a hedge fund you can use potentially more effective strategies which may put you into situations like that.

If i had any tether I would sell it all right now, on the off chance that tether is in fact not fully backed.

In the end there is no upside to holding it, so even small risk is unnecessary

Tethers collapse or fall from the peg would be such a contagion within the entire crypto ecosystem. I would think all crypto holdings are at risk if there are large adverse findings in the disclosure.

Theoretically, USDC is backed (or more backed) by dollars.

I'm not sure why anyone has ever held a Tether for even 1 second. Even if you believe in it 100% - why not hold something other people believe in more?

"Grant Thornton has switched from calling the $52.3 billion stablecoin’s reserve accounts 'correctly stated' to the more equivocal 'fairly stated.' Here’s why that matters."

I don't know why they all need to play this game. I guess because of their terrible performance after the IPO, they feel the need to make returns and using the reserves for riskier investments is just too tempting.

I'm surprised somebody like Chase hasn't started their own stablecoin and proven openly: we're backed 100% by T-Bills. We get some profit from holding your money, but it's small and safe. Why do they all have to be shady?

I suspect that if any bank tried to push out their own Crypto the Fed would have /Questions/ for them and in general it wouldn't work out well for the bank in question.

People don't hold tether because they love tether. They hold it because they need it to trade crypto. So you need to balance the risk of tether being a scam with the opportunity risk of not being able to trade because you don't hold it.

(This is an analogy, but it's almost literally the reality for a massive global market that not seen by the mainstream)

I'm not sure where you would read about it. It's like this... Bahamas dollars are pegged 1:1. They can be spent interchangeably in the Bahamas. You can redeem them 1:1 in the Bahamas. Very credible.

But most people are not in the Bahamas, and can't redeem them where they are. The Bahamas won't let just anyone in, and it's expensive to go there anyway. (Oh sure, if you're American and live in Florida it's no big deal, but if you're Chinese or Indian or something it's a big pain in the ass) There are money changers in other places that will take Bahamas Dollars, but they'll only take your B$100 notes and you're looking at like 4% loss to sell them, and for all your 20s, 10s, etc nobody will give you more than 50% for them if they will accept them at all. So these things are somewhat redeemable if you're in Canada or France... but in many places they are not redeemable at all.

Or you could use this other thing called Tether that just works. It costs 0.25-0.50% to turn into local currency if you're talking $10,000+ amounts. It can be done in almost place on Earth where you have running water and electricity.

GUSD is basically like B$. So given that reality, it's a no brainer to take Tether over GUSD, even if you think Tether is shady.

This is also something I didn't get about Tether for a long time... it's actually successful because its operators are shady, not in spite of it. They have been doing whatever it takes to maintain actual liquidity, and has done so for years. Gemini does not, it just sits there and brags about how it could totally pay everyone back if it wanted to.

Somebody has been redeeming huge amounts in the past 3 days, maybe someone knew what was up. You'd definitely want to redeem before they have to resort to those El Salvador IOUs at the bottom of the reserves pile.

The "honest" yield of on-chain lending protocols has decreased significantly through the year since it mostly came from lending to leverage traders. For example, USDC yield on Aave is down to ~2.8%, I think Compound's stable yield has been down to <1% for a while.

There are other sources of yield, such as Gemini Earn (6.5%), which lend to larger trading firms. Those feel riskier since they're more exposed to systemic collapse in crypto and lock up your dollars with a long withdraw delay.

Then there are the ponzi yields (10-40%), like the recently collapsed UST and the soon-to-collapse USDD and USDN. I think it's obvious why those are a bad idea.

Nit: Gemini's highest yield is 6.9% on their Gemini dollar stablecoin[1], and the withdrawal delay is promised to be at most five business days which they were able to adhere to (not that that's not long, depending on what you expect, just wanted to quantify) during last week's LUNA crisis.

I withdrew everything from Gemini Earn since I have no idea whether Genesis Trading, who borrows through Earn, would survive a significant loss of USDT peg.

USDC on Aave, Compound, or Curve all seem much safer.

Right but I'm only seeing pretty low interest on those platforms, which doesn't compensate for the risks of smartcontracts and going outside the usual financial system. Did you have a specific one you think is worth it?

For example, on Compound, USDC only pays 0.82%, or 1.3% if you count the COMP token rewards.

Also I don't think you can invest just in USDC on Curve, you have to do a pool that exposes you to some other currency, although I think DAI is solid and Curve has a cUSDC/cDAI pool:

...but rates have fallen already, I guess everyone is fleeing to stables and within stables everyone is fleeing to USDC. Current USDC rate is 1.46% (vs. 2% for USDT)

Right, that's where I went, and it didn't have the yields you represented, so I wasn't sure I found the right place.

Turns out I did find the right place, you just posted long-obsolete figures as fact without checking, in a thread where the actual values were the central point of discussion.

GUSD's site claims audits - under a heading titled "Review the Gemini dollar reserve-funds independent accountant audits" but links to attestations (example: https://assets.ctfassets.net/jg6lo9a2ukvr/3ZfEIugZkOLsArm4JK..., "conducted in accordance with attestation standards").

Same fraudulent trick Tether pulled for years. They're not the same thing.

Attestation: "Joe has $1,000 in the bank."

Audit: "Joe has $1,000 in the bank, but it's a loan from their brother, they just got fired, and a $2,000 mortgage payment is due tomorrow."

The main risk of being in that pool is that you might get stuck with GUSD which you would have a very hard time getting rid of unless you have an account with Gemini, and even then, I've heard of them refusing to redeem GUSD for USD to people who actually bought GUSD directly from them with USD.

The secondary risk of being in that pool is if any of the 3pool assets die. You'd have to hope to be automated enough to be out the door with the good ones.

Finally, the reward for being in there is the marketability of the CRV which is the lions share.

From what I can tell there is only a GUSD/3CRV pool. This means you will be exposed to GUSD, DAI, USDC, and USDT. If any of these depegs you will lose money because your DEPOSIT_AMOUNT USD worth deposit will turn into almost DEPOSIT_AMOUNT of whatever coin depegged. There is also risk of there being a vulnerability in a smart contract.

As an additional data point one of the higher yields for USDC alone seems to be based off doing a recursive lending strategy on Valas which at this current point in time has about a 6.9% APY.

Let's say it's 70% or even 50% backed. The withdrawals so far are are about 10% of its holdings. Won't we have to wait for another 40-60% draw down to find out if it's not fully backed? Seems like so far, anyone who wanted out, got out.

The question they seem to want to dodge is who is the issuer of all that Commercial Paper. They'd like people to believe it's a diverse group of blue chip companies. The reality is it's probably Binance and a few other crypto companies.

A great, laconic statement to rally the anti-crypto troops. In reality, destroying cryptocurrencies would have zero effect on any of those three:

Estimated total energy usage for all cryptocurrencies: 0.1-1% of global energy usage

Inflation: I don't see a link whatsoever - any influence on inflation from crypto is dwarfed by a decade of quantitative easing.

Labor supply: estimated number of developers working in crypto is <100,000, whereas estimates for total number of software developers in the world is ~20M, so ~0.5%.

While I agree with you on the last two points, this article from september last year[1], referencing this piece from the NYT[2], says that Bitcoin alone used 0.5% of the global energy used. 0.5% of the global energy consumption is an enourmous amount of energy, for one coin.

Even if it is only 1% in total, for all cryptocurrencies - 1/100 of the yearly energy used by the whole planet is a gigantic amount of energy, isn't it?

I agree that 1% (if true) is not insignificant, but destroying all cryptocurrencies to reduce our energy consumption by 1% isn't a clear tradeoff to me. We also need to account for the fact that renewable energy as a percentage of energy used by crypto is increasing and already at significant proportions.

So how exactly is this thing supposed not to look as scam?

Every news update I see suggests it is. Requests like this sound to me like "let us have our pretended peg/backing to pretend that out stablecoin is stable for a little longer".

If Tether is a fraud, I hope it collapses soon, so it can take down a bunch of other frauds within the crypto space and probably take at least a quarter of the inflated Bitcoin price down with it. Hold their feet to the fire.

Tether's market cap has declined about $9 billion in the past several weeks, going from ~$83B to ~$74B. If that continues, and its backing really isn't adequate, we will find out.

It allows people with less access to financial products to get around the gate keeping institutions and enjoy USD stability in countries where populations are financially restricted. Just like BitTorrent acts as a counterweight to a greedy entertainment industry, Tether acts as a counterweight to regimes who impose financial restrictions on their populations.

Stablecoins are the killer app that everyone has been waiting for. When implemented properly (with reliable and regulated backing) they allow people to build financial apps that easily transact real money, without paying a fortune to a payment provider. Combined with scalable blockchains, I suspect they’re going to be a huge force in the future payment/finance ecosystem. That future ecosystem may not look radically different from what we have today, it might even be most of the same players: but there will be different “rails” moving money at a lower cost, and new players that wouldn’t have been able to start up without this.

Disclosure: I don’t care much about stablecoins but I am working on regulatory compliance tech for decentralized currencies, and my instinct is that stablecoins are where all the business interest is.

Transacting USD requires access to legacy payment systems, such as the Federal Reserve's ACH. This system is heavily permissioned and requires a bank partner, with layers of middle-persons in between you and the Fed. It also runs on 1970s mainframe technology and has substantial clearing delays. This is currently the closest thing to an inter-party settlement system. Other payment providers exist outside of this, but don't have a great alternative to ACH for transacting between platforms, so they are islands with a few point-to-point bridges (think Venmo). Stablecoins potentially provide a fast and relatively permissionless platform to move USD (or other currencies) from owner to owner, essentially instantly. I think there are huge benefits to this and so stablecoin settlment will slowly "eat" the alternative systems as a result.

This is not to say that the transition will be straightforward. There are still many issues around transaction reversibility (ACH is reversible for a short period of time, due to trust relationships between banks) and fraud and money-laundering: not to mention that stablecoin regulation is still a work in progress and funds aren't FDIC insured. But I expect that some of these issues will get solved, and the tech will gradually replace ACH etc.

USD isn’t tokenized — it can’t be placed on a crypto wallet and transacted on a blockchain. So essentially you have to create a token that represents $1 in order to use real currency in crypto trading.

I'm not sure how you're avoiding that, especially once the stable coins are regulated? You still have payment processors to pay, just with different names

You may have heard of a country called Myanmar? Population of 54 million?

You might be surprised to learn that a citizen from Myanmar does not have access to a local bank offering USD accounts, nor do they get offers in the mail from Amex or Citibank. Their sole USD option may be holding cash under their mattress.

With a USD stablecoin, this citizen is no longer subject arbitrary exchange rates, expensive banks and risky currency storage. They can save money independently of any government or financial institution.

I have been wondering who the holders of Tether are, I really hope you are wrong. If people really are confusing the stability guarantees of the USD with a scammy cryptocurrency token like Tether, then it makes Tether lies all the more morally irresponsible.

Aside from optics, why doesn't a major central bank step in and create a stable-coin? A GBP/CAD/USD stable-coin collateralized by a central bank's reserves would be widely adopted at this point.

It's not clear to me why a major central bank would be interested in establishing a distributed currency that competes with their own centrally-managed currency.

Maybe it sort of possibly makes sense for a central bank in a small country where the politics are such that policy makers have decided to compete for the attention of the crypto industry. But a major central bank?

USD collateralized stable-coins are happening whether central banks participate or not. I think the advantage for a central bank would be to bring stability and increase demand for the underlying asset (the centrally controlled currency).

The conventional wrong answer is to short USDT/USD on an exchange like Coinbase.

The correct answer is to do a spread trade between BTC/USDT and BTC/USD since this is where the liquidity is.

The real answer for you is to stay away from this trade. If you need to ask how to do it, you obviously don't appreciate all the complications of such a trade. Remember that this trade will only make money if Tether implodes, and if that happens there will be crazy volatility all around, and you could end up losing money on a seemingly correct trade like shorting USDT/USD.

Most important is that you have to time the implosion, there's no obvious way to make a bet on Tether's eventual disaster without reference to when it happens.

So even if you consider it inevitable, backing that conviction with your own cash is a great way to get rekt.

The market can remain irrational for longer than you can remain solvent, and how certain are you that you'd be able to close out your short position when it did happen?

{kind=link}

Here's the actual source of documents in the case [1]: https://iapps.courts.state.ny.us/nyscef/DocumentList?docketI...

The most recent filing is the court's order granting Intervenor-Respondent Coindesk's Motion to File a Sur-Reply, which is a very procedural element.

Backing up: usually, in court cases, when there's an argument to do something, one party writes a brief, the opposing party writes its brief, and then the first party rebuts the opposing party's brief. Opposing party usually doesn't get a chance to rebut again. This order is letting the opposing party get that chance, and it was done because the first party made new arguments in its reply brief that it's not procedurally allowed to.

The court hasn't rejected Tether's bid to conceal the reserve records... it hasn't reached that point in the case yet. From the current posture of the case, I would guess that it's feeling more sympathetic towards Coindesk than towards Tether, but that really doesn't mean much in terms of what the actual ruling will be.

[1] Any news organization that doesn't provide a link to the actual docket when discussing cases should be considered irresponsible.